The United States, a global economic powerhouse, is currently wrestling with two significant economic issues: a banking crisis and inflation. These problems have not only affected the U.S. but have also reverberated throughout the global economy. This article aims to provide a comprehensive and in-depth analysis of these economic phenomena, exploring their origins, impacts, potential solutions, and the broader implications for the U.S. and global economies.

The Inflation Problem

The Genesis of Inflation

Inflation, in economic terms, refers to a sustained increase in the general level of prices for goods and services. As inflation rises, every dollar you own buys a smaller percentage of a good or service, which means the purchasing power of money decreases.

The genesis of inflation in the U.S. economy can be traced back to the economic disruptions caused by the COVID-19 pandemic. The pandemic had a profound impact on the global economy, causing widespread supply chain disruptions and labor shortages. These factors led to an increase in the cost of goods and services, which in turn led to inflation.

Supply chain disruptions occurred when factories around the world had to shut down or reduce their operations due to the pandemic. This resulted in a decrease in the production of goods, leading to a shortage in the market. At the same time, demand for certain goods increased as people adjusted to new ways of living and working from home. This imbalance between supply and demand drove up prices.

Labor shortages were another factor contributing to inflation. Many businesses had to close or reduce their operations due to the pandemic, leading to widespread job losses. As the economy started to recover, businesses began to reopen and rehire, but many people were hesitant to return to work due to health concerns or because they were receiving unemployment benefits. This led to a shortage of workers, forcing businesses to increase wages to attract employees. These increased labor costs were then passed on to consumers in the form of higher prices.

The government also played a role in the genesis of inflation. In response to the economic crisis caused by the pandemic, the government increased its spending to stimulate the economy. This included measures such as direct payments to individuals, increased unemployment benefits, and loans to businesses. While these measures were necessary to prevent a deeper economic downturn, they also increased the amount of money in circulation, which can lead to inflation.

Initially, the Federal Reserve, the central bank of the United States, believed that these inflationary pressures were temporary and would subside as the economy recovered from the pandemic. However, as inflation continued to rise and became more entrenched in the economy, it became clear that the problem was more persistent than initially thought. This led the Federal Reserve to take a more aggressive stance to combat inflation, including raising interest rates and reducing the amount of money in circulation.

The Federal Reserve’s Countermeasures

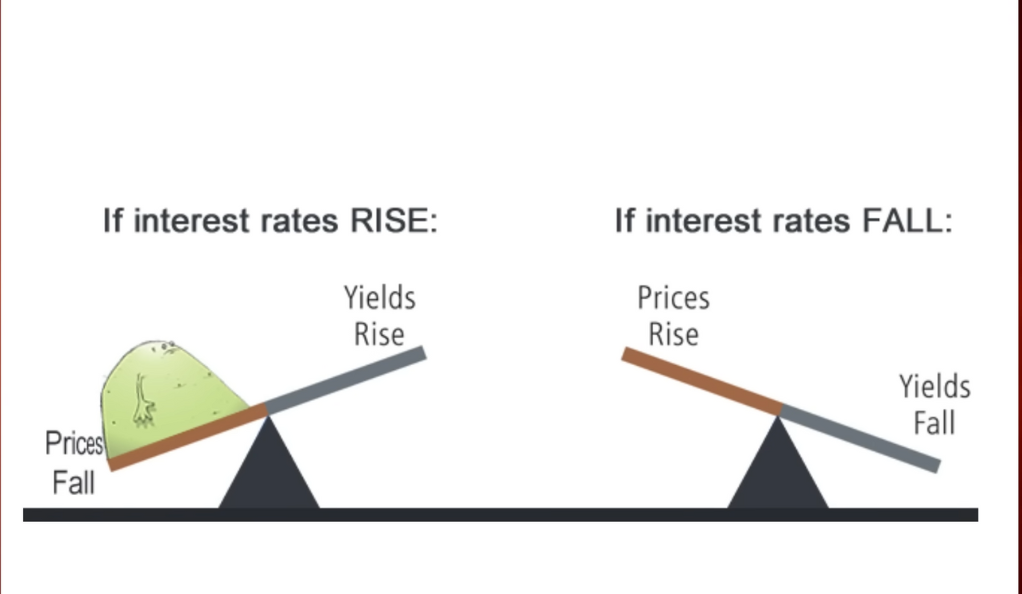

In response to the escalating inflation, the Federal Reserve decided to tighten monetary policy. This action involved raising interest rates aggressively. By increasing the cost of borrowing, the Federal Reserve aimed to slow down economic activity and curb inflation. This move was seen as a necessary step to stabilize the economy and restore consumer and investor confidence.

However, this aggressive tightening of monetary policy has had far-reaching implications, particularly for the banking sector. The higher interest rates have made borrowing more expensive, leading to a slowdown in economic activity and a decrease in the demand for loans. This, in turn, has affected the profitability of banks and other lending institutions.

The Banking Crisis

The Aftermath of Quantitative Easing

The U.S. economy had been conditioned under a policy of quantitative easing in the aftermath of the 2008 financial crisis. This policy involved the Federal Reserve buying bonds to reduce interest rates and stimulate economic growth. The idea was to make borrowing cheaper, encouraging businesses and consumers to spend more, thereby stimulating the economy.

However, the abrupt shift from zero interest rates to higher rates to tackle inflation led to significant economic shocks. Businesses and consumers, who had become accustomed to cheap borrowing costs, were suddenly faced with higher interest rates. This sudden shift has had significant implications, particularly for the banking sector.

The Collapse of Silicon Valley Bank

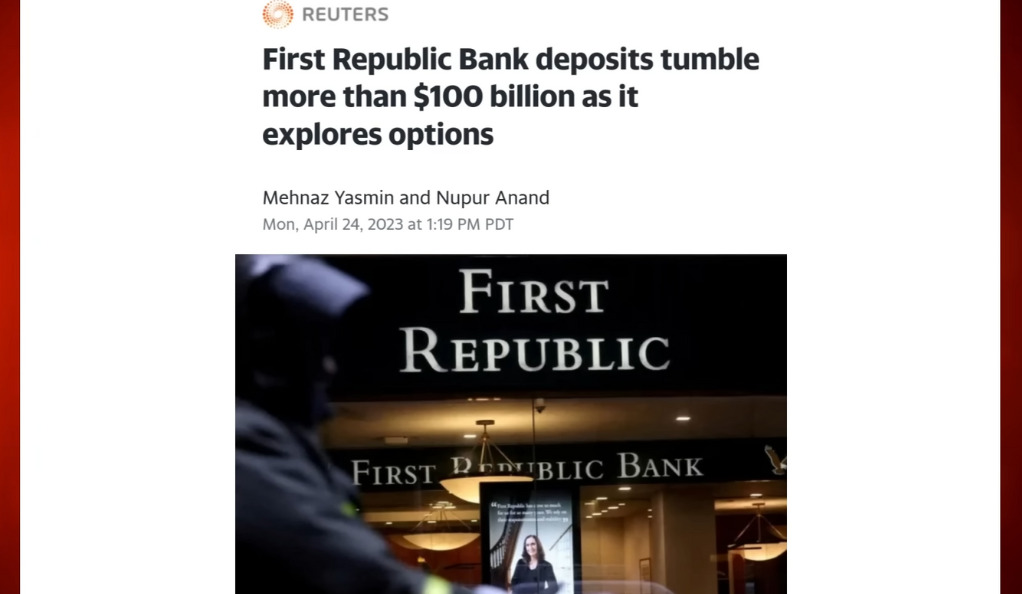

One of the most notable impacts of this shift was the collapse of Silicon Valley Bank. This event served as a stark reminder of the potential disasters that could arise from these economic shocks. To prevent a contagion impact, the Federal Reserve, the FDIC, and the Treasury Department extended lending facilities to banks. This move was aimed at providing a safety net for banks and preventing further collapses.

However, despite these measures, more bank collapses seem likely. For instance, First Republic Bank lost 40% of its deposits in the last quarter. Furthermore, U.S. banks are sitting on $1.7 trillion in unrealized losses. These figures paint a grim picture of the banking sector’s health.

The Impact on Banks and Consumers

The Struggles of Banks

Despite the safety nets provided by the Federal Reserve and other institutions, banks continue to struggle. The aggressive tightening of monetary policy has led to a significant reduction in the availability of cheap money, affecting banks’ profitability. Furthermore, the higher interest rates have led to a decrease in loan demand, further impacting banks’ bottom lines.

Moreover, the potential for further bank collapses remains high. Banks are not only grappling with reduced profitability but also with the prospect of significant deposit withdrawals. As interest rates rise, depositors may choose to move their money to higher-yielding investments, leading to a decrease in banks’ deposit bases. This situation is further exacerbated by the uncertainty surrounding the banking sector, which may prompt depositors to withdraw their money out of fear of potential bank collapses.

The Burden on Consumers

The tightening of lending conditions and the rise in interest rates have also had a significant impact on consumers. With inflation eroding their purchasing power and interest rates making borrowing more expensive, consumers are finding it increasingly difficult to maintain their standard of living. This economic squeeze has led many consumers to resort to credit card debt, which has hit a record of almost one trillion dollars. This trend indicates that consumers are feeling the pinch of the economic conditions, and their financial health is deteriorating.

Moreover, the rise in interest rates has also affected the housing market. Higher interest rates make mortgages more expensive, which could lead to a slowdown in the housing market. This could have a knock-on effect on the construction industry and other sectors linked to the housing market, potentially leading to job losses and further economic slowdown.

The Potential Recession

The Impact on Corporate Earnings

As consumers tighten their belts and reduce their spending, corporate earnings are expected to take a hit. Consumer spending is a significant driver of economic growth, accounting for about 70% of the U.S. GDP. Therefore, a reduction in consumer spending can have a significant impact on corporate earnings and, by extension, the overall economy.

The Threat of a Recession

The combination of reduced corporate earnings and the ongoing banking crisis could potentially lead to a recession. A recession, defined as a significant decline in economic activity spread across the economy, lasting more than a few months, could have severe implications for both businesses and consumers.

The wildcard in this scenario is whether commodity inflation will stick, leading to higher food and energy prices even in a wrecked economy. If commodity prices continue to rise, consumers could face even more financial strain, further exacerbating the economic downturn.

The Role of Government and Policy Makers

In the face of these challenges, the role of government and policy makers becomes crucial. They need to strike a balance between controlling inflation and maintaining economic stability. This may involve a combination of monetary and fiscal policies, as well as regulatory measures to ensure the stability of the banking sector.

Monetary policy measures could include adjusting interest rates and controlling the money supply. Fiscal policy measures could involve adjusting government spending levels and tax rates. Regulatory measures could include implementing stricter regulations for banks to ensure they maintain adequate capital reserves and follow prudent lending practices.

The Global Implications

The U.S. banking crisis and inflation problem have global implications as well. Given the interconnectedness of the global economy, a banking crisis in the U.S. could lead to a global financial crisis. Similarly, inflation in the U.S. could lead to increased prices globally, particularly for commodities and goods that are heavily traded on the international market.

Furthermore, the U.S. dollar serves as the world’s primary reserve currency. Therefore, changes in U.S. monetary policy and interest rates can have significant effects on global financial markets and economies. For instance, higher interest rates in the U.S. could lead to capital outflows from emerging markets, as investors seek higher returns in the U.S.

Conclusion

The U.S. economy is facing significant challenges, with the banking crisis and inflation problem causing widespread concern. The Federal Reserve’s response, while necessary, has led to economic shocks and potential bank collapses. Consumers are also feeling the impact, with many resorting to credit card debt to cope with rising prices. As we move forward, it’s crucialto keep an eye on these economic indicators and prepare for potential outcomes, including a possible recession.

Ainu Token aims to offer impartial and trustworthy information on cryptocurrency, finance, trading, and shares. However, we don't provide financial advice and recommend users to conduct their own studies and thorough checks.

{kind=link}

{kind=link}

Comments (No)